Hot Metal

Three things worth your attention this week.

Port Talbot's timeline just slipped, and the reason is instructive. Tata's £1.25 billion EAF — £500M of it UK government money — broke ground in mid-2025 at 3 Mt/yr with a claimed 90% cut in on-site CO₂. But in June 2026 CRU and Tata flagged a delay of up to a year, pushing first steel from end-2027 toward mid-to-late 2028. The cause isn't the furnace — it's the grid. National Grid has formally alerted Tata that the connection project (two substations, super-grid transformers, buried cable) is running late. The lesson repeats: for an arc furnace the power infrastructure is the critical path, and the scarce resource behind it is people who actually know how to run a DRI/EAF shop.

CBAM's definitive regime is live, and the paperwork has teeth. As of 1 January 2026 the transitional phase is over: importers over the 50-tonne threshold must be authorized CBAM declarants — the application deadline passed on 31 March 2026, with the first declaration and certificate surrender due by 30 September 2027 for 2026 emissions. The quiet part is that this is the front edge of the EU ETS free-allocation phase-out — the real cost lands on production, not just imports. If you sell into Europe, your embedded-emissions number is now a price, not a disclosure.

Default values just became the expensive option. Under the definitive regime, embedded emissions increasingly need verified actual data; fall back on defaults and you're charged as if you were among the dirtiest producers in your category. For low-carbon DRI-EAF operators that's backwards — your real number beats the default, but only if you can prove it. The plants that invested early in per-process emissions measurement are about to get paid for it.

Where the ton-of-product CBAM number gets modeled wrong

Most CBAM models we've seen are built by finance, not by the melt shop — and it shows. They treat the carbon cost as a tariff on imports and a disclosure exercise at home. Both framings miss what actually hits the cost sheet. Here's the operator's version.

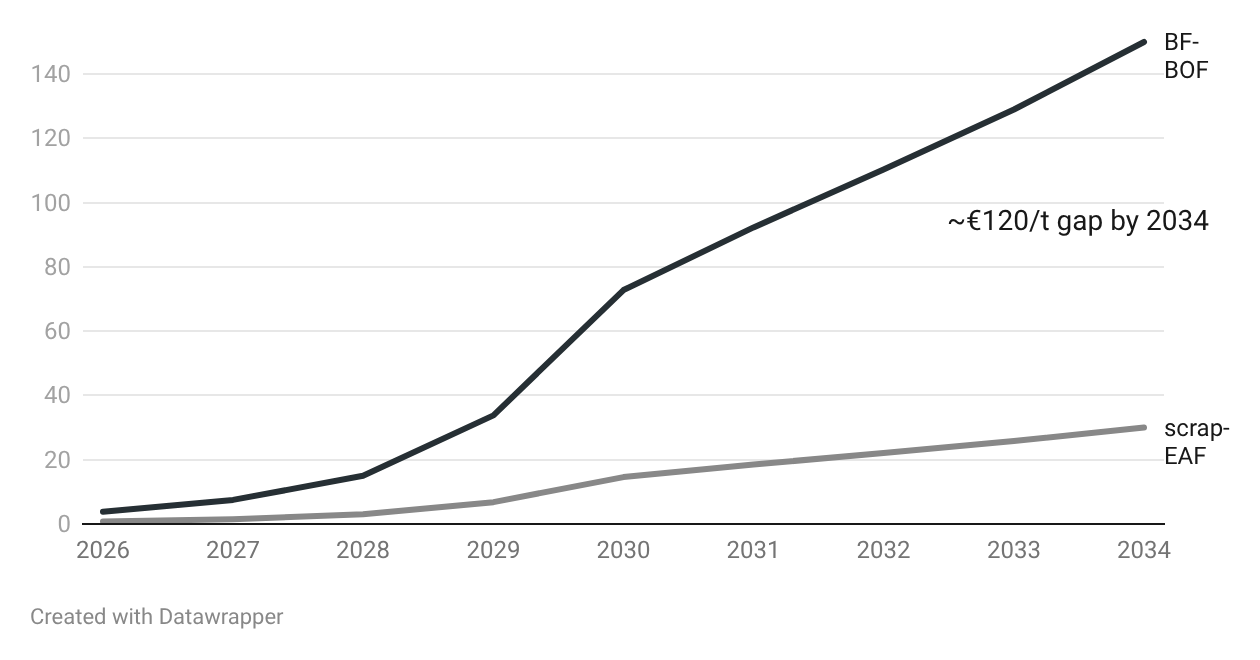

The mechanism is simple in shape: your cost is embedded emissions per tonne × carbon price × the share you actually pay for. That last term is the one finance keeps fixing at today's value, and it's the one moving fastest. The free-allocation phase-out runs on a published schedule — the CBAM factor climbs from 2.5% in 2026 to 48.5% by 2030 and 100% by 2034. So even at a flat carbon price, the cost per tonne of a high-intensity route rises roughly fortyfold across the window. Model it static and you're not wrong by a little. You're wrong by an order of magnitude on the back half.

Put real numbers on it. At a carbon price around €75/t CO₂, integrated BF-BOF steel at roughly 2.0 t CO₂/t carries an eventual carbon cost near €150/t of steel once free allocation is gone — squarely inside the €100-170/t range the published analyses quote. A scrap-EAF at roughly 0.4 t CO₂/t lands near €30/t on the same basis. That €120/t gap is not a rounding error; it's a structural moat, and it widens every year on the schedule. The chart traces both curves from 2026 to 2034 so you can see exactly where the lines separate.

Where the modeling goes wrong, specifically:

Treating it as an import tariff. The bigger hit for most EU-selling producers is their own rising ETS bill as free allowances disappear — CBAM just stops importers from undercutting that. Model your own production cost first.

Fixing the carbon price and the phase-out factor. Three terms move: intensity, price, and the CBAM factor. They compound. A spreadsheet on 2026 assumptions understates 2030 by a wide margin.

Ignoring indirect and precursor emissions. For an EAF, the grid emission factor behind your power and the embedded emissions in purchased DRI/HBI and pig iron can dominate your number. Leave them out and your "low-carbon" claim won't survive verification.

Banking on default values. Defaults are deliberately punitive. For a genuinely low-intensity DRI-EAF, they can cost you the entire advantage you actually have — but only verified actual data unlocks the real figure.

The strategic read: a low-intensity route used to be an ESG talking point. On this schedule it turns into a hard cost advantage that compounds every year the high-carbon competition pays more. But the advantage is only real if you can prove the number — measured, verified, per process. That proof is a data problem, which is why the next section is a list, not a lecture.

Operator's Notebook — 7 data sets to start collecting now for CBAM

If you'll need a verified emissions number per tonne, start the trail now. Retrofitting a year of history is the part nobody budgets for.

Direct process emissions, measured per process step, not back-calculated from annual fuel totals.

Electricity consumption per tonne, paired with your supplier's grid emission factor — the indirect number CBAM increasingly wants.

Embedded emissions of purchased iron units — DRI/HBI, pig iron — from supplier documentation, not assumptions.

Reductant and carbon inputs (natural gas, injected carbon, electrodes) with their CO₂ factors.

Per-heat mass balances, input to output, so emissions can be attributed to product correctly.

Production tonnage by product type, mapped to the CN codes the way CBAM reports them.

The monitoring methodology and verification trail itself — documented now, so an auditor's first question isn't your last scramble.

The plants that can produce this trail on demand will price their carbon advantage into every contract. The ones that can't will pay the default and watch the moat work against them.

Next week: predictive maintenance on a DRI shaft — where it actually returns the investment, and where it's an expensive dashboard.

Written by active DRI-EAF operators. Anonymous by necessity, specific by design.