Hot Metal

Three things worth your attention this week.

ThyssenKrupp's hydrogen plan is sliding to gas-first. They paused the green-hydrogen supply tender after the offered prices came in well above plan, while the Duisburg DRI plant — 2.5 Mt/yr, hydrogen-ready — keeps moving toward a natural-gas start, with hydrogen penciled for 2028 and 100% operation in 2029. The molecule isn't ready; the furnace is. Build the DRI shaft now, feed it gas, switch to H2 when it pencils — that ordering is becoming the real European playbook, whatever the press releases say.

China is building the H2-DRI base it intends to export from. Baowu commissioned a million-tonne hydrogen DRI-EAF line in Zhanjiang in late 2025 and announced a roughly $1.5 billion green-hydrogen hub at Yangjiang; HBIS runs the other large-scale hydrogen plant at Zhangjiakou. The tell is that Baowu still leans on grey hydrogen from coke-oven gas — which says everything about how hard fully green H2-DRI is to commercialize, and how fast the learning curve runs once it's at scale. Watch the technology going overseas, not just the tonnes.

The EU ETS free-allocation clock started. Free allocation for steel drops 2.5% this year, 5% in 2027, nears half gone by 2030, and hits zero in 2034, with CBAM phasing in at the matching rate. Analysts put the eventual carbon cost at €100-170/t on BF-BOF steel at current ETS prices. For DRI-EAF operators that's the structural tailwind: the carbon delta you've always had over the blast furnace just turned into a number your integrated competitors have to write a check for.

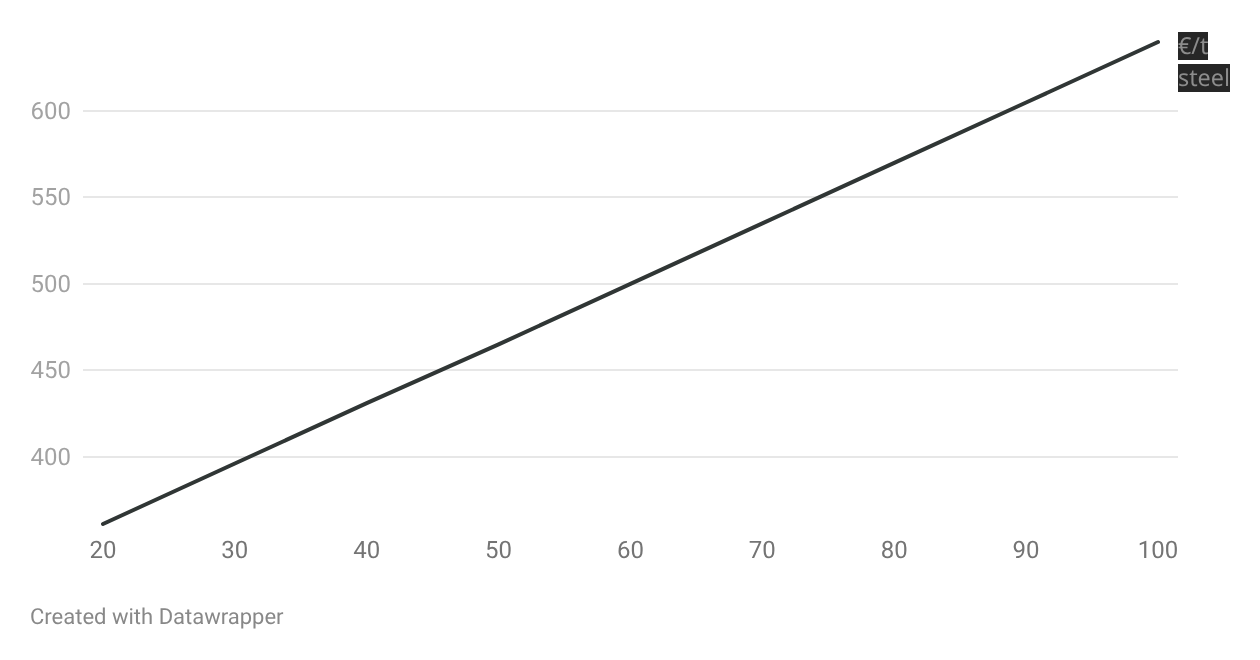

The number that decides H2-DRI isn't capex

Every green-steel announcement leads with capex and a ribbon-cutting date. The number that actually decides whether H2-DRI works is duller and almost never quoted: the capacity factor of the electrolyzer feeding it.

Here's the mechanism. Green hydrogen cost is mostly amortized capex on the electrolyzer plus the electricity to run it. Run that electrolyzer flat-out and you spread its capital over a lot of kilograms. Run it only when power is cheap — say a 30-40% capacity factor chasing low spot prices — and you spread the same capital over far fewer kilograms. The €/kg of hydrogen swings hard on that one choice, and because hydrogen is the dominant variable cost in H2-DRI, the €/t of finished steel swings with it.

That's the tension nobody resolves cleanly. Cheap electricity wants a low capacity factor — only run when renewables are abundant and prices crash. Cheap hydrogen wants a high capacity factor — amortize the electrolyzer. You can't have both without either oversized storage or firm low-carbon power, and both of those put the cost right back on the €/t line you were trying to protect.

The chart puts a number on it. The canonical assessment of the route (Vogl and colleagues, 2018) pegs H2-DRI at roughly 3.48 MWh of electricity per tonne of steel — which turns every €10/MWh move in power price into about €35/t on the steel, and puts total cost anywhere from around €360/t on cheap power to €640/t on expensive. Capacity factor sits underneath that: chase the cheapest spot power and your €/MWh falls, but the electrolyzer capex you're now amortizing over fewer running hours pushes back the other way. Same lever, two ends — and the spread is wider than most operators' entire margin.

Now put scrap-EAF next to it. A scrap-fed EAF melting cold charge has no iron-ore reduction step and no hydrogen bill at all — its cost is scrap, power, and electrodes. H2-DRI exists because there isn't enough quality scrap on Earth to make all the world's flat steel, and because some grades need the clean iron units DRI provides. But on pure cost today, scrap-EAF wins on variable cost in almost every scenario, and H2-DRI only closes the gap when carbon is priced — which is exactly what the EU ETS phase-out above is now doing on a fixed timetable.

So the honest read on Stegra's first heat, when it comes: the heat itself proves the metallurgy, which was never really in doubt. What it won't prove is the economics. Those depend on the power contract behind the electrolyzer, the capacity factor they can actually sustain, and the carbon price their customers' alternative pays. First heat is a chemistry result. The capacity factor is the business result, and it shows up quarters later, in the cost report, not the press release.

The takeaway for operators isn't "root for hydrogen" or "root for scrap." It's that the iron-unit decision — scrap, gas-DRI, H2-DRI — is now an energy-contract decision as much as a metallurgical one. The shops that win this decade treat their power and carbon position as a process variable, not a line on someone else's spreadsheet.

Operator's Notebook — 4 design decisions that make a DRI plant H2-ready

If a DRI shaft might run hydrogen later, four choices made now decide how cheap that switch will be:

Reformer bypass / shaft gas flexibility. Design the reducing-gas circuit so the H2 fraction can rise without re-tubing the shaft. Retrofitting gas handling later is where "hydrogen-ready" plants quietly aren't.

Metallization control at higher H2. Hydrogen reduction is endothermic and shifts the thermal profile. Make sure your metallization control and heat input have headroom before you need it, not after.

Carbon-in-DRI strategy. More hydrogen means less carburizing gas, so the carbon you hand the EAF drops. Decide early whether you protect EAF carbon with feed carbon or recipe — it changes melt energy downstream.

Electrolyzer-to-shaft buffering. Even modest hydrogen storage decouples a variable-capacity-factor electrolyzer from a shaft that wants steady gas. Size it deliberately; it's the cheapest insurance against the cost curve above.

These aren't exotic engineering. They're the gap between "H2-ready" on a slide and a shaft that actually takes the switch without a second capital project.

Next week: CBAM 2026, read from the melt shop — what the carbon border actually does to a tonne of your steel, and who pays.

Written by active DRI-EAF operators. Anonymous by necessity, specific by design.